The baby bust will not destroy our pensions, unless we allow it to

The baby bust will not destroy our pensions, unless we allow it to

Blaming the low birth rate for undermining UK pensions obscures the flaws of recent pensions reform - and is based on a misunderstanding of what pensions provision is

Pensions provision in the UK has been undergoing a process of individualisation for decades. You are responsible for your own financial future – and what you put in is what you get out.

But this was only ever surface-level individualisation, orchestrated to release employers from their traditional responsibilities for their employees’ welfare in retirement.

Beneath the surface, it is impossible to individualise pensions (as I argue in my book Pensions Imperilled). Even in an individualised ‘defined contribution’ scheme - effectively a personal pension - the whole thing only works if your savings are combined with the savings of thousands of others, to enable the kind of investment returns your future pension depends on.

Furthermore, when you reach retirement, most people will dissolve their savings into an annuity (a regular income for life) via an insurance company – the insurer is only able to provide this because it has perhaps millions of other customers doing the same, allowing risks to be shared and priced.

At a more fundamental level, private pensions provision of any type only works if the providers are confident that future cohorts will behave in roughly the same way as today’s savers. Without the likelihood of long-term profitability, there is no incentive to build and maintain the financial architecture of pensions saving.

And from the investment perspective, the assets that our pensions are invested only retain value if there are future investors willing to buy them from us at some point.

The fall

Everybody who knows anything about the business of pensions knows all of this, but it has become increasingly difficult to talk about it, as the ideological climate emphasises only what the individual chooses to do, or not do, as the explanation for retirement outcomes.

Until now.

The myth that we are on our own is swiftly cast aside when it seems the real foundation of pensions provision – the ability of future generations to keep replenishing the system with cash – is jeopardised.

The revelation that the UK’s birth rate is continuing to fall has inspired concern that, with a smaller cohort of workers paying into pension schemes in the future, the promises made to today’s pensioners (and soon-to-be pensioners) might be unaffordable. So much for personal responsibility, eh?

But the apparent jeopardy to our pensions has been over-stated, based on a simplistic, accountancy-based understanding of pensions provision. At the very least, we cannot be sure what impact the baby bust will really have. Pensions provision is invariably designed around financial forecasts that never come to pass.

The last couple of years have given us a tragic reminder in this regard. The actuaries did not account for many thousands of pensioners dying earlier than they otherwise would have as a result of COVID-19 – effectively a ‘windfall’ gain for the providers committed to lifelong pension payments.

They also did not anticipate the pandemic encouraging people to delay starting a family, or deciding not to have additional children. Moreover, increasing life expectancy in the UK (i.e. hitherto one of the main causes of population ageing) has now gone into reverse (irrespective of COVID-19). Yet we are lumbered with a pensions system transformed in the mid-2000s based on the assumption that life expectancy would never stop rising.

The failure of the future to align with our projections is seen as a problem for pensions in the neoliberal imaginary. In my view, however, this uncertainty is precisely why capitalism needs decent pensions provision. A guarantee that we will be taken care of in later life, whatever the future holds, is essential to the reproduction of labour.

Value

And this is why we need the state must be at the heart of providing guaranteed pensions. Yet the UK has one of the lowest value state pensions among OECD countries. Only the state is ultimately able to withstand the inherent uncertainties involved in protecting the value of our pensions many decades into the future.

Outsourcing the role to individuals themselves is fallacious. This role was outsourced to large employers for a while (i.e. ‘defined benefit’ provision), for some workers – and there are few good reasons this should not continue. But state provision should be the central pillar of retirement income for most people.

The falling birth rate has given rise to fears of a shrinking tax base when the smaller cohorts reach adulthood, undermining the state pension’s sustainability. Tax revenues from working-age people finance pensions in payment, de jure and de facto. But this fatalism is unwarranted. The tax base can and should change – most obviously, by rebalancing toward taxing wealth ahead of income.

Family drama

So, the impact of the falling birth rate has been over-stated, and there are countervailing trends at play too. Even if the impact did manifest, associated risks can be managed by the state. But I think we need to go further, and unpick the notion that a low birth rate will endure, and that it would necessarily be disastrous for pensions provision if it did.

The low birth rate – which is not unique to the UK – appears to have three main causes. First, personal choice, which policy-makers rightly have little control over (whatever Paul Morland may think). This includes the impact of the pandemic on family planning, but perhaps also the spectre of climate catastrophe. Save the planet to save our pensions, I guess (but maybe save the planet, either way).

Second, lower net migration after the implementation of Brexit (associated also with COVID-19’s impact on international travel). We can assume this trend will persist for at least a while: the UK is willingly failing to import the people of child-bearing age that we need.

Third, a stagnant economy, denying young people the financial security which tends to precede parenthood. And poor pay (alongside student debt for some) and limited security is being combined with greater work intensity, which hardly helps.

There are specific economic problems for potential parents contained within this broader picture, such as the inaccessibility of home-ownership for many (especially in London), and the astronomical cost of childcare (which tends to inhibit people with children having larger families).

The greater good

Pensions and parenthood are similar in this regard. They might look superficially like the product of something going in, to allow something to later come out. But they both work best when the wider economy is in a healthy state.

Growth helps. But a good economy also means one in which:

employers provide decent pay and conditions;

capital is allocated to long-term value-creation (such as the technologies and infrastructures supporting green transition) over rent-seeking;

foundational industries such as care are organised as a public good; and

good housing is available and fairly priced for all.

In my view, this kind of economy will grow more strongly. Irrespective of this, it would certainly be good for pensions provision, directly enabling higher contributions and more stable investments.

In the case of housing, it also takes some of the pressure off pensions provision; people who have paid off mortgages by the time they retire can manage on lower incomes in later life. Instead, we are sleepwalking into an epidemic of retired renters.

Destiny

Demography is not destiny.

We can choose to have more inward migration, just as we can choose decent and affordable early-years provision. We can choose to have the kind of economy that will enable and sustain decent retirement outcomes.

Other things being equal, of course, it is better to have more people helping to finance the pensions of the already-retired. But other things are never equal.

The baby boomers have seemingly used their political and economic power to secure their own financial interests. Yet the boomer cohorts are extraordinarily unequal, with millions lacking access to a decent pension.

The younger boomers (aged mid-50s to mid-60s) are facing particularly difficult challenges in this regard. This ‘forgotten generation’ risks being the first victim of large-scale pensions individualisation, with many having lost access to defined benefit pensions at a much earlier life-stage than older boomers (mid-60s to mid-70s).

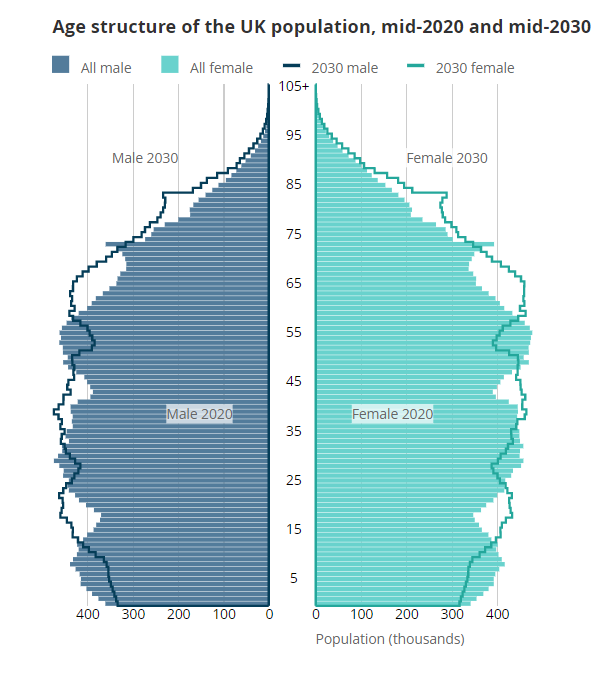

The great irony, of course, is that pensions individualisation was set in train amid another baby boom, roughly early 1980s to late 1990s, as the large post-war boomer cohorts started families (this is visible in the age pyramid above). Life expectancy was of course increasing - but it had been increasing for decades. The demographic foundations of collectivist pensions (both state and occupational provision) were therefore generally sound.

Yet the pensions promise was dismantled, piece by piece, and replaced by a system where the only promise we make is to ourselves. Millions of twenty- and thirty-somethings could have been helping to fund decent pensions for their parents, but have been denied the opportunity to do so. No wonder the boomers (well, those that were able to) saw fit to hoard housing wealth instead. This will be passed on to their pensionless kids in due course, transmitting class-based inequality across the generations.

So here we are. If a high birth rate was not sufficient to prevent the retrenchment of collectivist pensions, then a low birth rate is no reason not to fight for their restoration. If it does end up undermining pensions provision as it stands, then the incentive to pursue ambitious reforms should be even stronger.