Understanding – and misunderstanding – economic policy institutions

Understanding – and misunderstanding – economic policy institutions

The purpose and operations of the Treasury and the Bank of England are not very well understood, so I did something about it

I conducted a study (funded by the Friends Provident Foundation) recently on what undergraduate students are taught about economic policy institutions, such as the Treasury and the Bank of England, on typical economics and political science degrees in UK universities.

I found that they are not taught very much! Economics students might learn about the functions of institutions such as central banks, but not the history, structure, organisation, personnel, political relationships, and prevailing ideas or foundational assumptions of these institutions.

You might expect political science to do a better job on this, given its inherently critical gaze at the life of policy institutions, but economic policy in particular is barely included at all within the core content of a typical degree.

This post is not really about the problem which I studied (I will write more on this in future), rather the solutions I devised.

I compiled a series of introductory papers for use on undergraduate degrees across the social sciences. And I’d hope they would be useful to non-academics too: policy practitioners, journalists, the general public, etc.

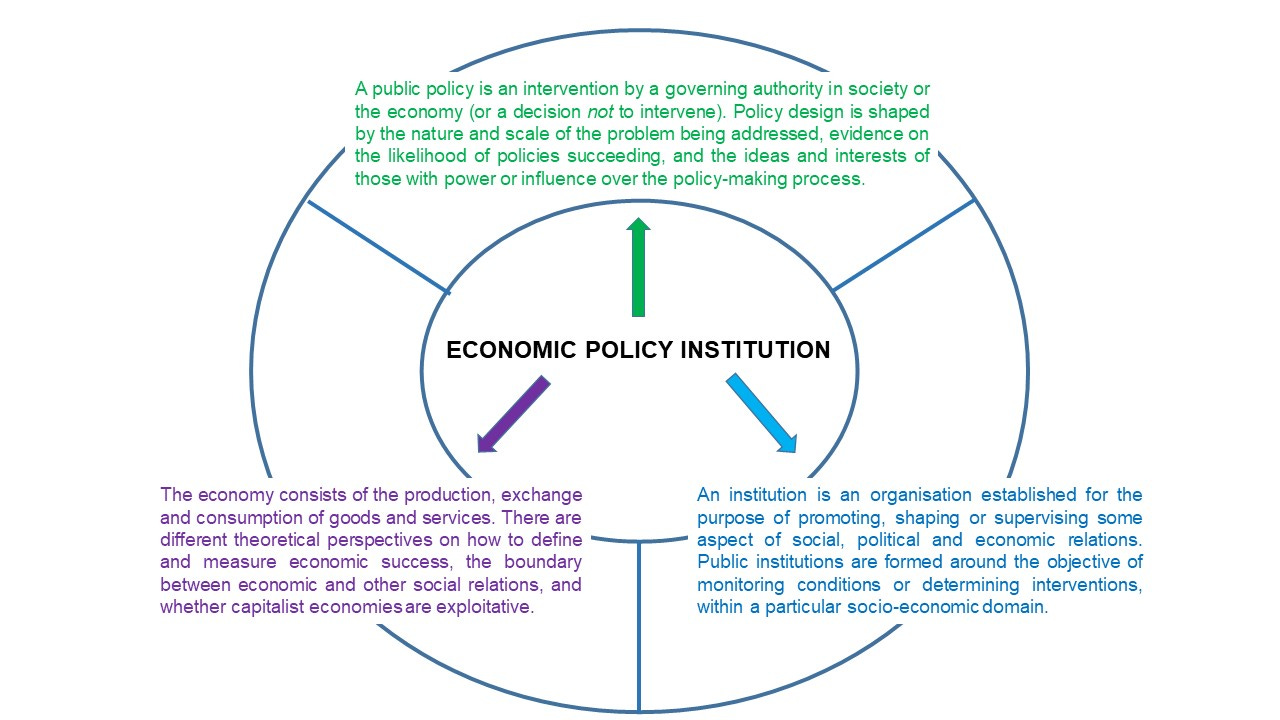

The first explored what economic policy institutions are, and how to analyse them.

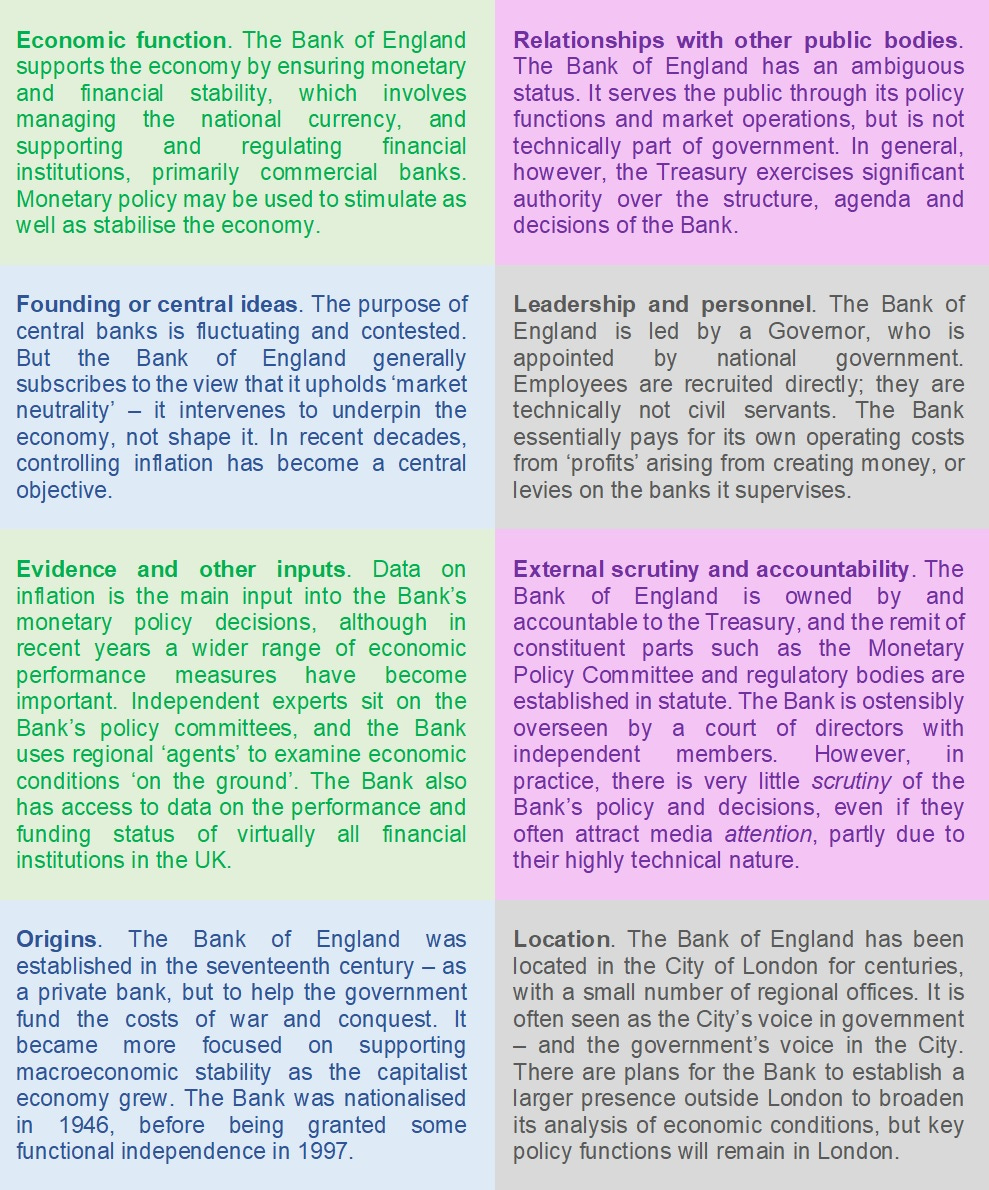

The second was focused on the Treasury, and the third on the Bank of England. Below I’ve included a preview of both: tables summarising the key characteristics of each institution. The full set of resources is hosted on the Rethinking Economics website – this includes an accompanying set of essays by leading experts on the two institutions, and some learning exercises which might help to bring the documents alive in the classroom.

The Treasury and tax cuts

I have been thinking about this project this week because of the Johnson government’s apparent enthusiasm for placing tax cuts at the centre of its economic policy agenda.

It is easy to explain this as ‘the same old Treasury’, reverting to type. I even sort-of succumbed to this myself, in a post on the abandonment of the ‘levelling up’ agenda.

But it shows how little the Treasury is understood if we assume that it automatically favours low taxes. Its main preoccupation is fiscal risks: the state taking on responsibilities which will require high levels of public spending. This is the better explanation for its reluctance to sanction interventionist economic policy. But tax cuts are also a fiscal risk, since they undermine the state’s revenue base.

(The Laffer curve – which suggests that lower tax rates lead to higher tax revenues – may be theoretically attractive to some at the Treasury, but is generally irrelevant to most tax decisions.)

While it is correct to assume that the Treasury enjoys considerable power among Whitehall departments, it is the limits to the power of Treasury mandarins which are not widely understood. A historical reading of the department would suggest that Chancellors of the Exchequer (especially if they are supported, or at least tolerated, by the Prime Minister) have considerable scope to shape Treasury decisions, and indeed the day-to-day work and structure of the department.

It is probably fair to say that there are ideological commitments which recur in the Treasury’s agenda over the long-term. But this is most evident when these commitments align with the political interests of the Chancellor.

The Bank of England and inflation targeting

Ironically, the Bank of England’s ideological commitments are probably more firmly rooted into place than those of the Treasury. Yet the institution is seen by most as an entirely technocratic institution, free of ideological bias.

Frustratingly, political scientists actually use the Bank of England’s independence, granted in 1997, as an example of policy-making becoming more technocratic, or depoliticised (the only time the Bank is substantively discussed in undergraduate teaching). But this really is not what is going on at all.

Price stability is a good example.

Controlling inflation is arguably in the DNA of all central banks, and the Bank of England has led the international consensus on inflation targeting – as the key objective of monetary policy – for decades.

The Bank of England invariably tends to see inflation as a demand-side issue. Essentially, the expectation is that, if inflation begins to rise, monetary policy (i.e. higher interest rates) will be used to restrict credit, therefore aggregate demand, and ultimately wages (with wage rises conventionally considered to be the main source of inflation).

It is of course rather convenient for the institution that this understanding of inflation justifies the importance of monetary policy, the Bank’s main policy function – as well as the central bank’s independence from elected governments who fear the wrath of voters.

Again, however, this commitment is not unwavering. The Bank’s previous (and only foreign) governor, Mark Carney, called inflation targeting ‘a destructive distraction’. He had, of course, presided over the period in which very low interest rates – accompanied by the creation of lots of new money through quantitative easing – had not had any significant impact on inflation.

Yet now that inflation is rising sharply in the UK (as elsewhere), it is the Bank which has reverted to type.

Current chief economist Huw Pill said upon his appointment last year:

I looked at this institution from the outside and I was always pretty convinced it is in the price stability business… I’ve come inside, as is the nature of entering institutions, you’re surprised by some things while others confirm you’ve expected. One thing that is totally confirmed is that [the Bank] is an institution that’s in the price stability business.

All the evidence suggests that the inflation we are currently experiencing is a supply shock, caused by the pandemic, Brexit, and Russia’s invasion of Ukraine. But the Bank has other ideas.

Not only is the Bank raising interest rates in order to restrict demand, current governor Andrew Bailey has asked workers to voluntarily snuff out demand, by forgoing pay rises even as their earnings plummet in real terms.

This clearly does not represent the unbiased application of economic knowledge. It is a deeply political perspective, shaped by the intellectual, industrial and geographical landscape in which the Bank has been situated for centuries.

All of these policy issues deserve to be discussed at greater length. My argument here, essentially, is that we cannot begin to understand the policy decisions they result in, unless we understand the complex nature of the institutions within which these decisions are being made.