The Shared Accommodation Rate: the flawed benefit that many need but few claim

Housing cost support for young people is based on a fiction. Youth homelessness is the inevitable outcome

Almost half of people in England who were assessed as homeless, or threatened with homelessness, in 2022/23 were aged 16–34. The number of under-25s seeking Citizens Advice support with homelessness issues has increased by 18,700% in the past ten years, and 25-34 year-olds have overtaken both 45-54 year-olds and 55-64 year-olds in this grim league table.

We know well some of the structural drivers of this trend. Young people experience low pay and employment insecurity. Mental health is a huge problem. Affordable housing is under-supplied, and landlords in the private rented sector have too much power over the lives of their tenants. Policy can and should address all of this, but even if a new government dedicated itself to the task, the problem would not be turned around quickly.

We need the welfare state to step in sooner. If not now, when? Yet the flawed design of housing cost support for 16-34 year-olds is exacerbating rather than alleviating this situation.

History

If you are aged between 16 and 34, do not live with a partner, and do not have children, the government expects you to rent a single room in shared housing, if you need support with covering your housing costs.

The ‘shared room rate’ (SRR) was first first introduced in 1996. It became the ‘shared accommodation rate’ (SAR) in 2008 when Local Housing Allowance (LHA) was introduced in order to restrict Housing Benefit expenditure. LHA linked Housing Benefit maximum amounts (and now Universal Credit housing element maximum amounts) to rent costs in the area where claimants lived: they could only receive housing cost support up to the value of the median rent in their area.

For the SAR, this meant the median cost of renting a single room in shared housing. The SRR and the original SAR applied only to under-25s. It may of course be a reasonable assumption that living in shared housing reflects a transitional lifestage between living with immediate family to fully established adulthood. In 2012, however, the upper age limit was increased to 35: the same lifestyle assumptions cannot be applied to people aged 25-34.

At the same time, the LHA maximum was reduced to the 30th rather than 50th percentile of local rents. And even this less generous approach to uprating was hardly ever applied, with LHA only uprated by CPI, 1%, or frozen altogether, most years after 2012.

The four-year freeze from 2020 onwards, while the cost of living — and specifically the cost of renting — rose dramatically was particularly harmful.

Cause

My recent report with Ed Pemberton, however, argues that, even if the SAR had remained tied to local rent costs, the policy’s flaws would still be negatively affecting young people.

The most obvious is the fact that there is far too little shared housing available: demand outstrips supply, almost everywhere, especially in terms of affordable properties priced at or around the SAR. People are being forced to live beyond their means.

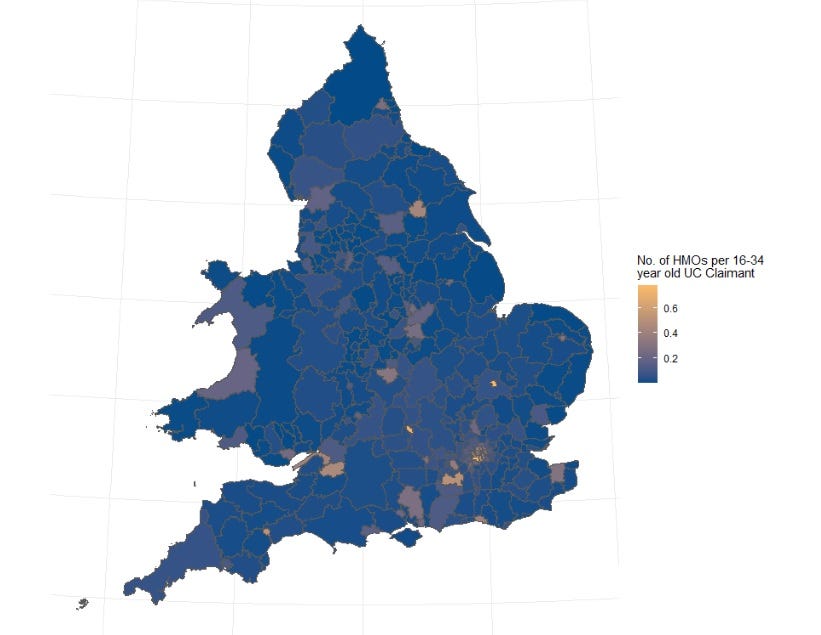

The map below shows the number of houses or flats of multiple occupancy per person aged 16-34 in England and Wales:

The issue looks even starker when we take into account the places where young people on Universal Credit actually live:

Partly as a result of the limited supply of shared housing, and partly because of the way rent data is collected by the government, extraordinarily few data points (i.e. actual rent being paid in shared housing) are included in calculations to find the 30th percentile of local rent costs, compared to other LHA rates.

And the data that is collected seems to include student accommodation, which is generally cheap but not accessible to typical benefit claimants (this artificially deflates the SAR, and under-states the shortage of shared housing in areas with large universities).

The calculation of the SAR is therefore unreliable. The small number of data points means the rate is volatile too. And the time it takes to collect rent data, followed by an implementation lag, means that the rate applied in April 2024 is actually based on rents in payment between October 2022 and September 2023 (this is a problem for all LHA rates).

It is also worth noting that, even where affordable shared housing is available, it is not suitable for all. People who are neurodivergent may find it difficult to share with strangers. Refugees granted leave to remain are expected to find a home in a very short amount of time, but often lack the social networks that people rely on to access shared housing.

And separated parents who do not have main custody of their children are not supported to provide a suitable family home for the nights they are caring for their children. None of these groups are covered by the SAR’s narrow range of exemptions.

Effect

The most glaring effect is the shortfall between housing cost support and actual housing costs that people on the SAR experience. 88% have a shortfall between support and their actual rent. This compares to 64% for all Universal Credit housing element claimants in the private rented sector. This is because many will be living, by necessity, in more expensive property types.

In the last financial year, people on the SAR receiving debt advice from Citizens Advice had an average monthly shortfall between their rent and the level of support they received of almost £250. This is nearly £100 higher than the average monthly shortfall (£157) faced by people across other LHA categories.

The real impact, however, is on the people who do not claim housing cost support at all — because they would have no way to cover the shortfall.

To the nearest thousand, we now know there were 112,000 people receiving housing cost support at the SAR level in November 2023. This is significantly below the 150,000-300,000 estimate that Ed and I came up with, based on a caseload of 198,000 ten years earlier (there was much better caseload data available publicly for Housing Benefit compared to Universal Credit, so we had to FOI the more recent numbers).

Why is the 2023 caseload so much lower?

There is no demographic explanation: the number of people aged 16–34 today is almost identical to the number in 2013.

There is no labour market explanation: the claimant count for 16–34 year-olds (a measure of the number of people claiming out of work benefits) was lower in November 2013 than in November 2023. People in work can also claim housing cost support, and the switch to Universal Credit has made this much easier, so we would have expected caseload numbers to go up, not down.

Lesson

The optimistic conclusion is that, now that LHA, including the SAR, has finally been uprated, more people will become eligible for housing cost support, and the caseload should increase.

This should not, however, be taken for granted. The flaws are too significant. Uprating will not lead to more (affordable) shared housing options becoming available, and will at best only mask problems with how the SAR is being calculated. Note also that, as things stand, LHA will be frozen again, indefinitely, from 2025 onwards. A new government will be faced almost immediately with deciding whether to stick to this plan.

And the stakes are too high. In addition to contributing to homelessness among young people, the SAR is preventing many more from building an independent life (and finding work). The missing caseload is likely to include people not receiving housing cost support because they are still living with their parents (this is already the most common living arrangement for the 1.5 million 16–34 year-olds receiving Universal Credit). They have a roof over their head, but not a home of their own.

Notwithstanding the structural housing market reforms required, the SAR must be urgently reformed to prevent the housing crisis getting worse for young people in the meantime.

A Labour government should abolish it. At the very least, the upper age limit should be reduced to 25 (in line with the original policy).

Whether the upper age limit is 25 or 35, we need to introduce mechanisms to increase the SAR, such as setting payments at the halfway point between the SAR as calculated and the one-bedroom rate of housing cost support, or indeed linking the SAR to median rents again.

Additionally, there is a need to widen the range of exemptions to the application of the SAR, and ensure Discretionary Housing Payments — provided by local authorities, but funded centrally, to help people at risk of homelessness — are more available to young people affected by the SAR.

The SAR is a textbook case of poor policy design, with assumptions about how a certain group should live clashing with the reality of the narrow range of choices available to this group.

It is also a clear example of the damage austerity has done, and is still doing, with the small savings resulting from tweaks such as increasing the upper age limit to 35 and reducing the uprating reference to the 30th percentile (and then failing to apply it anyway) not justifying the devastating and often unseen impacts these measures have had.