Productivity puzzles and monetary policy mysteries

The bluntness of monetary policy as a tool of macroeconomic management is increasingly clear: the UK economy is almost beyond help

With thanks to the glacial pace of academic publishing, I published this week the outcomes of a study on the impact of low interest rates in the UK — several months after the central bank began increasing rates sharply in the hope, apparently, of controlling inflation. Yet the factors driving investment behaviour identified by the research (conducted alongside John Evemy and Ed Yates, and funded by the ESRC’s Productivity Insights Network) remain salient. In this post, I summarise the study, and reflect on what it tells us about the current turn in monetary policy practice.

The post argues that, after a decade and a half of getting almost everything wrong, there is, finally, some light at the end of the tunnel for UK economic policy. But it might of course be too late to reverse the significant living standards correction the UK is now experiencing. And there remain impediments within economic policy thinking — including on the centre-left — which derive in part from a misdiagnosis of the cause of the post-2008 malaise. In short, demand is at least as important as supply in generating a productive and innovative economy — and monetary policy increasingly seems part of the problem, not the solution.

I’m starting to think UK economic policy-makers might not know what they’re doing

Productivity has (rightly) been a fixation of UK economic policy-makers since 2010. The results of all this hoo-ha have been underwhelming. Productivity levels measured by GDP per hour have remained largely stagnant over this period, as has labour productivity per hour. This outcome is a marked change from the 50 years before, wherein labour productivity grew slowly but steadily at an average rate of around 2% per year across the whole economy.

Has the Conservative government, in office for 13 years and counting, produced a single policy which responds to this trend with anything like the seriousness required?

The Labour opposition has only occasionally floated an alternative agenda which corresponds to the scale of the challenge. Yet there does now appear to be a new supply-side agenda emerging which eschews the usual tools of tax cuts and deregulation, in favour of an active state thinking seriously about shaping and making markets.

Yet, as George Dibb has argued, ‘supply-side reform can never be the entirety of the solution to the economic malaise that the UK faces if demand remains suppressed’. Supply-side interventions must operate in parallel, not in opposition, to supporting demand.

We are not yet where we need to be. Frankly, however, anything would be better than the muddled thinking that has characterised UK economic policy since the financial crisis. Alongside several abortive attempts at both deregulatory and interventionist supply-side reform, economic policy-makers have relied principally upon (extraordinary) monetary policy — i.e. very low interest rates and quantitative easing — to restore economic growth.

This approach has been focused, ostensibly, on both demand and supply. On the one hand, monetary radicalism has sought to compensate for the impact of fiscal contraction — deemed necessary to protect the public finances — on demand. Yet it was also designed, on the other hand, as a supply-side intervention, insofar as cheaper credit would enable more private investment.

What the research tells us: even when we get around to investing, we’re getting it wrong

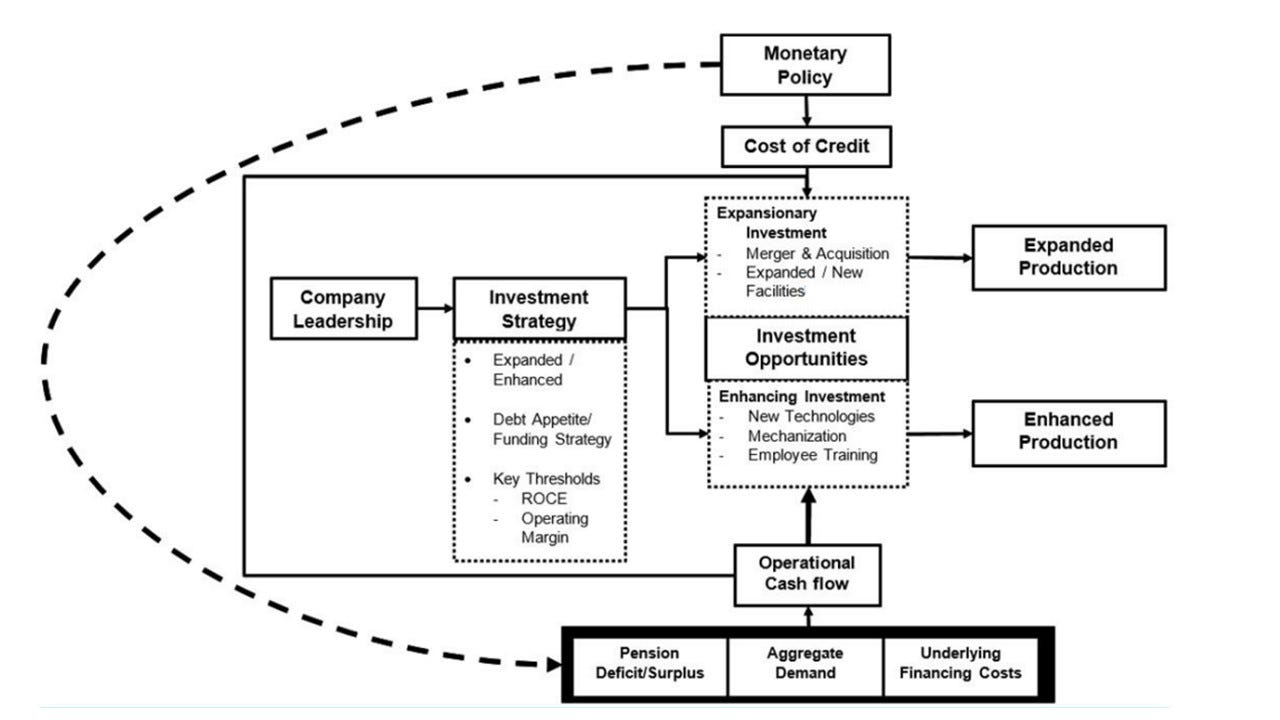

It is this latter claim that my research with Evemy and Yates sought to investigate. In what we think is one of the first studies to attempt to isolate quantitatively the direct impact of monetary policy on investment strategies, we asked how firm financing strategies shape investment behaviour in a very low interest rate environment.

To answer this, we sampled FTSE250 firms across two broad sectors for a mixed-methods study on how credit conditions in the period 2012-2016 encouraged firms to invest in either enhanced or expanded production (ending in 2016 because of the more volatile investment conditions since the Brexit vote). The former is defined as the adoption or development of new technologies, and improving sites and processes of production, and the latter is defined as applying existing techniques at a large scale, via a larger workforce or new sites of production.

Accordingly, an enhanced production investment strategy will increase the firm’s productive capacity and therefore, other things being equal, contributing to increasing productivity at the aggregate level. But an expanded production investment strategy is unlikely to boost productivity and could be deflationary as firms use cheap funds — in combination with a flexible and lightly regulated labour market — to grow without being required to become more efficient.

Our most important finding was that extraordinary monetary policy has very little direct effect on firm-level investment strategies (corroborating a qualitative Federal Reserve study of US firms). In fact, operational cash flow served as the main source of investment funding. Generally speaking, it is investment strategies which drive firm financing models, rather than vice versa. We identified a lack of a direct connection between how a firm funded its operations, including how it utilises credit, and its strategic investment decisions.

This does not mean that low interest rates did not facilitate certain forms of financing. As such, it is clear that the use of external financing to fund investment is more strongly associated with expanded production investment strategies rather than productivity-enhancing investment strategies.

Among the sampled firms, both expansion- and enhancement-focused firms engaged in the refinancing of existing debt at longer terms to fund investment. However, expansion-focused firms were more likely to use low long-term borrowing costs to, for example, acquire other firms and new production facilities. Accordingly, low interest rates directly facilitated scalar, often lower-margin, investments and acquisitions, but did not directly facilitate productivity-enhancing investment.

It’s not supposed to be like this…

The interviews we conducted with firm executives help us to understand why external finance is associated with expanded rather than enhanced production investment strategies. Productivity-enhancing investments are generally seen as ‘business as usual’. So investors expect this to be funded by ‘internal’ cash flow (not least because such processes, and their outcomes, are also more difficult to quantify). On the other hand, expansion is seen as more exceptional, and so can be funded from external finance.

As one director in the construction industry told us:

I think as business leaders we’re very reluctant to go and spend money on R&D or new technology or improving facilities unless we’ve got the capital structure to do it, within the firm, rather than going out and borrowing money to do it that you then think is going to increase productivity.

The implication is that, other things being equal, firms which are already performing well are more likely to be able to invest in enhancing productivity. Of course, relatively few firms are performing well at the moment. The ‘business as usual’ approach to efficiency gains has actually become a rather unusual sight in UK plc.

There are two big take-aways here. The first is the realisation that we are still failing to address the UK’s chronic under-investment problem.

But the second is that, insofar as we are, to some extent, facilitating investment, we tend to facilitate the wrong type of investment. Thus the chronic productivity problem endures, which adds to the unattractiveness of the UK economy as an investment destination.

We are inflicting a downward demand-supply spiral on ourselves, for no particular reason

The supply side needs investment. But the demand side drives investment in the private sector. This is almost never acknowledged in proposals for more muscular industrial and innovation policy (although it is not exactly unknown to economists).

In theory, price inflation helps to incentivise investment; real interest rates are lower than nominal rates, and loans are easier to repay. It is not good for demand though, unless incomes inflate too. There are no ideal solutions here, but increasing taxes on the wealthiest to help to mitigate inflation, while supporting the purchasing power of those more likely to spend in the real economy, is the least-worst way of supporting demand (as well as being the fairest way by far). (And we should be clear that demand-side interventions can induce higher inflation, if companies simply take the opportunity to increase prices: this is precisely why supporting demand must be accompanied by a robust programme of supply-side reform.)

The UK seems more set however on allowing inflation to deepen economic stagnation. The government is seeking to prevent incomes keeping pace with rising prices, by both imposing real pay cuts in the public sector, and offering only limited help to benefit recipients (despite the fact that lower-income households experience a higher inflation rate).

The Bank of England, for its part, is doubling down on an arcane orthodoxy at the worst possible time. While the UK economy remains afflicted by a lack of demand among low- and middle-earners, the Bank’s go-to solution is to further discipline and punish workers. This might help to control inflation, eventually. But the Bank’s destination is rather hazy: it is doing what it always does, because something must be done. It is not wrong, of course, to worry about the value of sterling — an objective the central bank never quite acknowledges — but wrecking the economy is a rather odd way to tackle this.

There are two things worth noting here. First, the (in)correction the Bank is imposing will be painful, but it will be slow and painful, rather than quick and painful as hoped. The Bank expects to make millions of households significantly worse off, but the impact will only materialise over several years due to many mortgage-holders enjoying fixed-rate mortgages for the time being (the proliferation of which was, ironically, due to the previous folly of very low interest rates).

In other words, inflicting a recession in order to control inflation is not as easy as it used to be.

Second, where demand is being depressed by higher interest rates, rather than leading to lower inflation in any straightforward way, we are in fact only making the economy more vulnerable to inflation driven by supply shocks. The UK needs to enhance its domestic productive capacity (especially as its terms of trade rapidly deteriorate), including in renewable energy generation, so that it is more insulated against production shortfalls elsewhere.

But this means more private investment, driven in part by demand. In attempting to avert a barely identifiable wage-price spiral, economic policy-makers are risking a downward demand-supply spiral.

There are a few things we could try…

My research with Evemy and Yates, while focused on a period of low inflation, perhaps therefore helps us to understand how we got to where we are now, or at least why the UK has been among the worst affected countries in terms of inflation. Simply, the failure to invest in productivity means we had it coming.

The situation is not hopeless. As well as focusing on supporting demand, so that firms can reorient to the ‘business as usual’ approach of reinvesting their profits in their productive capacity, we advocated:

Significantly increased public investment, as part of an industrial policy programme — we should not really be trying to do the latter without the former. (Note that the government’s decision to fund nominal public sector pay rises from existing budgets will almost certainly see UK public investment fall further, as departments raid their capital budgets.)

A more discerning approach to business finance, essentially through public investment banks — we have to stop seeing public banks as somehow unBritish, and provide credit intelligently, at a larger scale, to drive productivity growth.

Corporate governance reforms which, for example, give workers a stronger voice in investment strategies — this will help to mitigate against investment strategies with suppressed labour costs being seen as the default.

It would probably be worth adding here that:

Demand from overseas is of course a key part of this picture — we desperately need to find a way of reopening the UK economy to our main trading partners.

In the case of products at the green technological frontier, the state itself may have to take on the role of customer, breaking the path-dependencies in consumer and business behaviour holding up decarbonisation.

So... not hopeless, but not easy. Implementing the agenda above would represent an almighty task for an incoming government. Labour is already promising some of this stuff — and may go further once in power.

Yet Labour’s agenda is also being held back by its commitment to certain fiscal rules, which the shadow chancellor Rachel Reeves acknowledges are driven by electoral considerations (which is obviously fair enough, if she’s right: you can only govern if you win).

A rule requiring a falling debt-to-GDP ratio over the medium term may be an unnecessary barrier to the scale of public investment now required (although Labour is also considering a net debt calculation which encompasses public assets as well as liabilities). And a rule that dictates the government can only borrow to invest will hinder efforts to support demand: it will be necessary to challenge an arbitrary distinction between investment and day-to-day spending to prevent this.

In terms of monetary policy, we need on the one hand to introduce a broader set of tools, both to control inflation, and to address the coming climate crisis which will inevitably make inflation — and everything else — considerably worse. The Monetary Policy Committee can play an important steering role in this regard, as well as retaining operational independence on the base rate, albeit with the committee’s composition and targets reformed.

On the other hand, we need to recognise the limits (and flaws) of monetary policy, returning fiscal and industrial policy (and indeed social policy) to the fore in the hope of pulling the UK economy back from the brink. As Adam Tooze’s analysis of the US inflation experience suggests, monetary policy can help to address inflation, while (massive) fiscal expansion helps to address some of its causes — and allowing real wages to rise. The key is for fiscal and monetary policy to work in tandem.

A modern economy circulating products and services throughout the world doesn’t need money or sovereign countries (national currencies) to be successful. Today, we’ve the scientific knowledge and technological skills to convert our natural and artificial resources into daily, life-sustaining deliverables: food, housing, education, healthcare, infrastructure, employment, and other important demands. What we lack is unity, a global framework built upon fair and humane laws and safe and healthy industrial practices. I hypothesize that humanity can end poverty and reduce pollution by abandoning wealth and property rights, and instead adopt and implement an advanced resource management system built to provide “universal protections for all”. Replacing traditional political barriers altogether, this type of approach, which I named facts-based representation, allows us a better way to govern ourselves and our communities. In other words, collective decision-making processes based on the latest information that, in turn, improve the outcomes impacting our everyday personal and professional lives.

#ScientificSocialism