Farewell to the Cost of Living Payment, one of the best ever bad policies

Farewell to the Cost of Living Payment, one of the best ever bad policies

Offering a brief glimpse into the welfare state's future, the Cost of Living Payment did more good than we tend to assume

The Cost of Living Payment (CoLP) is no more. Devised in 2022 to help low-income households with the impact of inflation, final payments were distributed in February this year.

The policy survived four Chancellors and three Prime Ministers; introduced by Rishi Sunak when he was the first of the former group, and abolished by him when he was the last of the latter.

It was a bad policy. And it did quite a lot of good.

What?

The first round of payments began in autumn 2022. Over two instalments, recipients of most means-tested benefits received £650. There was also a one-off £150 CoLP for people on non-means-tested disability benefits, and £300 for all pensioner households (both could be received in addition to the main CoLP).

The second and final round of payments began in spring 2023. The main CoLP linked to means-tested benefits was increased to £900, with payments to disabled people and pensioner households kept the same.

Over the two years the CoLP operated, it cost around £20 billion in total, although only around £13 billion was allocated to means-tested benefit recipients. By comparison, the UK spends around £80 billion each year on means-tested benefits.

Why?

The CoLP was a direct response to the post-pandemic inflation surge. Means-tested benefits rose by 10.1% in April 2023, but this almost two years after inflation began to rise sharply. The CoLP was needed partly because of inflation, and partly because the UK welfare state is so bad at addressing inflation.

Due to a long implementation lag, benefits had risen by only 0.5% in April 2021, and 3.1% in April 2022. And uprating was only partially applied. Means-tested benefits for housing costs were frozen between 2020 and 2024 even as rents rose sharply. The two-child limit, overall benefit cap and specific cap on housing cost support all limit the income of families in receipt of benefits. The Consumer Prices Index under-estimates living cost increases for the poorest households.

And so it was that the CoLP came to be: a recognition of the regular system’s inadequacy. At the same time, however, the policy served to soften demands for more permanent reforms.

When?

The CoLP attracted two main criticisms. First, in addition to being time-limited by design, its dissemination system meant it offered only temporary respite against inflationary pressures.

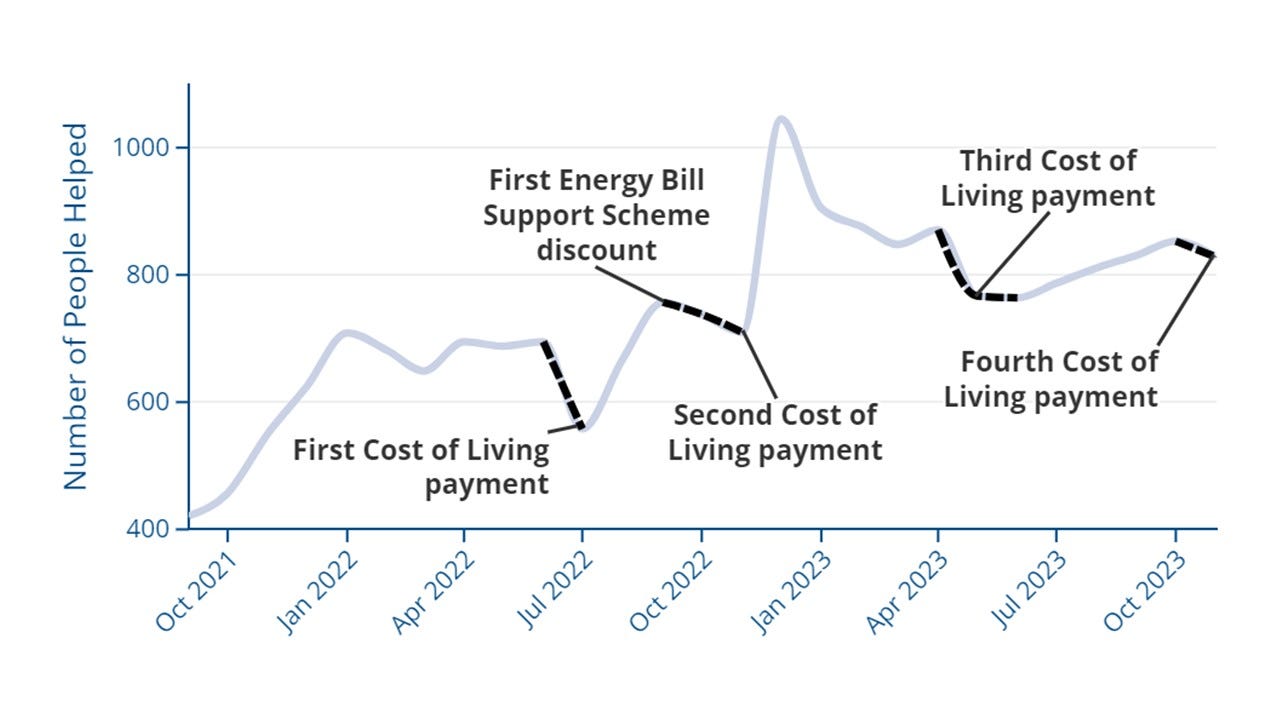

This is clearly evident in Citizens Advice data on the number of people the charity helped with food bank referrals each day:

The chart above shows that daily referrals dipped during the period the two payments in 2022/23, and the first two of three in 2023/24, were being distributed. But the upwards trend then quickly resumed.

The implication is that CoLP income was used to meet immediate needs — like having sufficient food to eat — but had no lasting positive impact on the financial position of recipients.

A cynic might conclude that it would have been better if the value of these sporadic transfers had been spread across weekly or monthly benefit payments instead, restricting the possibility they would be immediately spent. A more humane conclusion would be that sparing people of the need to use food banks, even for just a couple of weeks, was better than a small uplift in regular payments that would have left many people unable to meet their family’s basic needs most of the time anyway.

Either way, the main problem here is not the CoLP, but the fact that something like the CoLP was needed at all.

How?

The second main criticism was that the CoLP was poorly targeted. Of course, means-tested benefits are targeted on those out-of-work or with very low earnings — so CoLP targeting errors to some extent reflect imperfections in the underlying system.

The worst examples of the CoLP’s deliberately poor design were:

The failure to differentiate payments by family size: a means-tested benefit recipient with no children would be receiving lower benefits income than a household with several children, but they would both receive the CoLP at the same level. This design of course compounded the appalling and ineffective two-child limit and benefit cap, both of which penalise larger families.

The exclusion of people receiving only Housing Benefit (compounding the decision to freeze its value, noted above).

The failure to include people eligible for but not claiming means-tested benefits — especially when benefits such as Pension Credit have such low take-up rates.

Universal Credit has a low take-up rate too, among people who would only be eligible for a small award. But let’s be clear: being eligible for even a pound of Universal Credit each month means you are a low-income household. Complex rules and uncaring administration might have discouraged you from applying for a regular means-tested benefit income, but does this mean you also deserved to miss out on support totalling £1,550 while inflation ran riot?

Of course, the government argued that relying on existing means-tested benefit records enabled the CoLP to be distributed quickly and largely seamlessly (it also pointed to the creation of the time-limited Household Support Fund for those who might have missed out).

This constraint does not excuse the Housing Benefit oversight; this cohort could perhaps have received a lower payment. And it does not mean that families in receipt of the Universal Credit child element or Child Tax Credit could not have straightforwardly received a higher payment.

The government also decided to exclude people with nil awards in Universal Credit within the CoLP qualifying period. This group included people with a fluctuating income (often on a zero or low-hours contract, or self-employed) who happened to have earnings that took them out of benefit eligibility at just the wrong time, but usually need Universal Credit to supplement their income. It also included people for whom sanctions have temporarily reduced their Universal Credit payments to zero, therefore inflicting a double punishment.

The CoLP was the ultimate sticking plaster policy: struggling against a tide of inadequacy, attempting to compensate for a flawed system while relying on this system in order to function.

What the…?

And yet, somehow, for a large number of people, the CoLP worked.

The latest data shows that poverty rates got significantly worse from 2021/22 to 2022/23. But they would have been worse still without the CoLP. The chart below shows the 2022/23 absolute and relative poverty rates, after housing costs, for working-age adults, children, pensioners, and people living in families with at least one disabled person. Crucially, it also shows Department for Work and Pensions estimates for what poverty rates would have been had there been no cost of living support measures that year.

(Note that cost of living support included energy bill and council tax discounts as well as the CoLP.)

These percentages are real people. For example, there would have been 200,000 more children in relative poverty, and 300,000 more in absolute poverty, without the extra support. They were still poor, just above the poverty line, but less poor than they would have been.

Children actually benefited less from the CoLP than pensioners and disabled people. This is unsurprising given the additional payments for these groups (with many also receiving the main CoLP) and the failure to increase the CoLP with family size. But this probably only serves to underline the good the CoLP could have done, if addressing child poverty had been a higher priority in its design.

Now what?

Ideally, the CoLP would have continued into 2024/25: an election year. Partly because extra support is still needed. And partly because it would be advantageous if a new government inherited both the CoLP mechanism and its budget line. It would be politically difficult for a Labour government to abolish something a Conservative government was doing to make people slightly less poor, at least not without promising to spend a similar amount on something equally worthy.

Labour might have ended up keeping the CoLP indefinitely, like its derided ancestor the Winter Fuel Payment. But the typical policy wonk struggles to tolerate badly designed policies, no matter how effective for — and popular among — the ordinary folk who actually benefit. So there was very little resistance to the CoLP’s demise. We are only ever one think-piece away from technocratic utopia, I guess.

Could the £20 billion have been better spent? Yes, without a doubt. But we might just have had to rewire the British state, and its political and intellectual circuitry too, in order to do so.

Benefit levels need to be a lot higher, rebalancing towards universal payments as well as improving outcomes within the means-tested safety net. Poverty would be minimised and productivity would improve. But even in this scenario — indeed even if the hallowed Universal Basic Income were introduced — there are going to be more economic crises that undermine the adequacy of any welfare transfers. Climate change means unpredictable disruptions to production processes and recurrent inflation surges.

In this context, levels of contractual benefits of any type are likely to be lower not higher in the future in countries like the UK. This will protect the fiscal space needed for discretionary support like the CoLP.

The uplift to Universal Credit payments introduced during the COVID-19 pandemic was never going to be repeated by a Conservative government so soon, in fear that it would have become increasingly difficult to unravel. But the CoLP meant that the cost of living crisis could be put on furlough, at least for a moment.